April 2025

In this article, we ask how global regions are supplied with diesel generator sets, and look at what's produced in-region and imported from other regions.

The short answer is that this is driven by the economics of component supply and by the desire to be located close to major markets.

There are several key success factors for producers of diesel generator sets and one of the most important is the location of production facilities. Two factors often decide this.

Location of Major Component Suppliers

Diesel generator sets contain a high percentage of bought-in components. Engines, alternators / AC generators, cooling systems, control panels and other items can account for most of the manufacturing costs of a basic open unit. The labor element in putting it all together is actually quite small, often a single digit percentage cost on a basic open unit at a lower power rating.

This means that producers of diesel generator sets work closely with major component suppliers and locate production facilities nearby. It's more efficient and keeps costs down.

Near to Regional Opportunity

It's not surprising that producers are located where there is significant market opportunity.

Proximity to both suppliers and customers means lower costs and shorter lead times. And therefore North America, Europe, China and India are all major global production powerhouses.

Major components account for a large percentage of manufacturing costs for diesel generator sets.

As far as possible, producers of diesel generator sets aim to locate production facilities near to major suppliers.

The Genstat database from Parkinson Associates identifies production and market opportunity for diesel generator by 12 power bands.

For simplicity, in this analysis we'll look at 3 bands:

7.5 - 1500 kVA (split into 7.5 - 250 kVA and 251 - 1500 kVA)

> 1500 kVA

7.5 - 1500 kVA

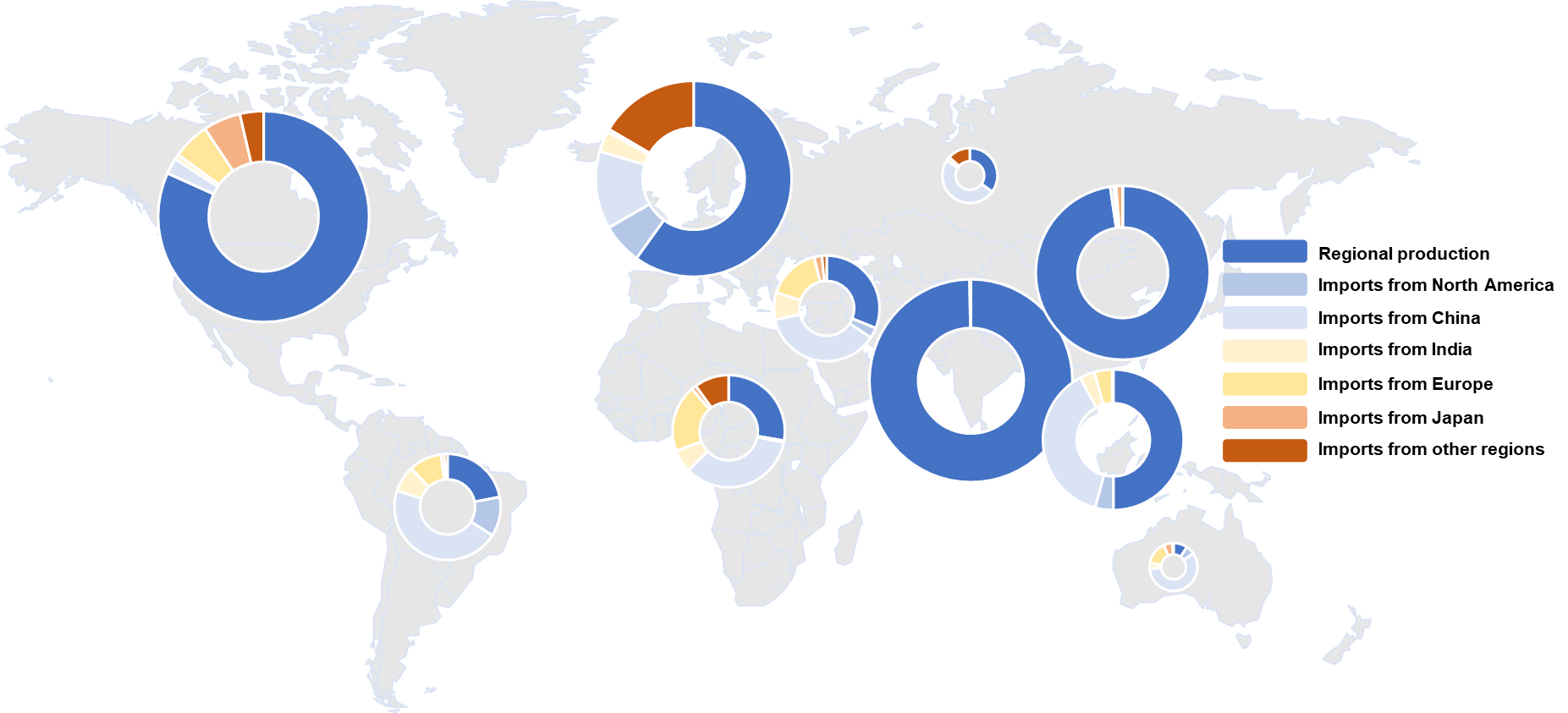

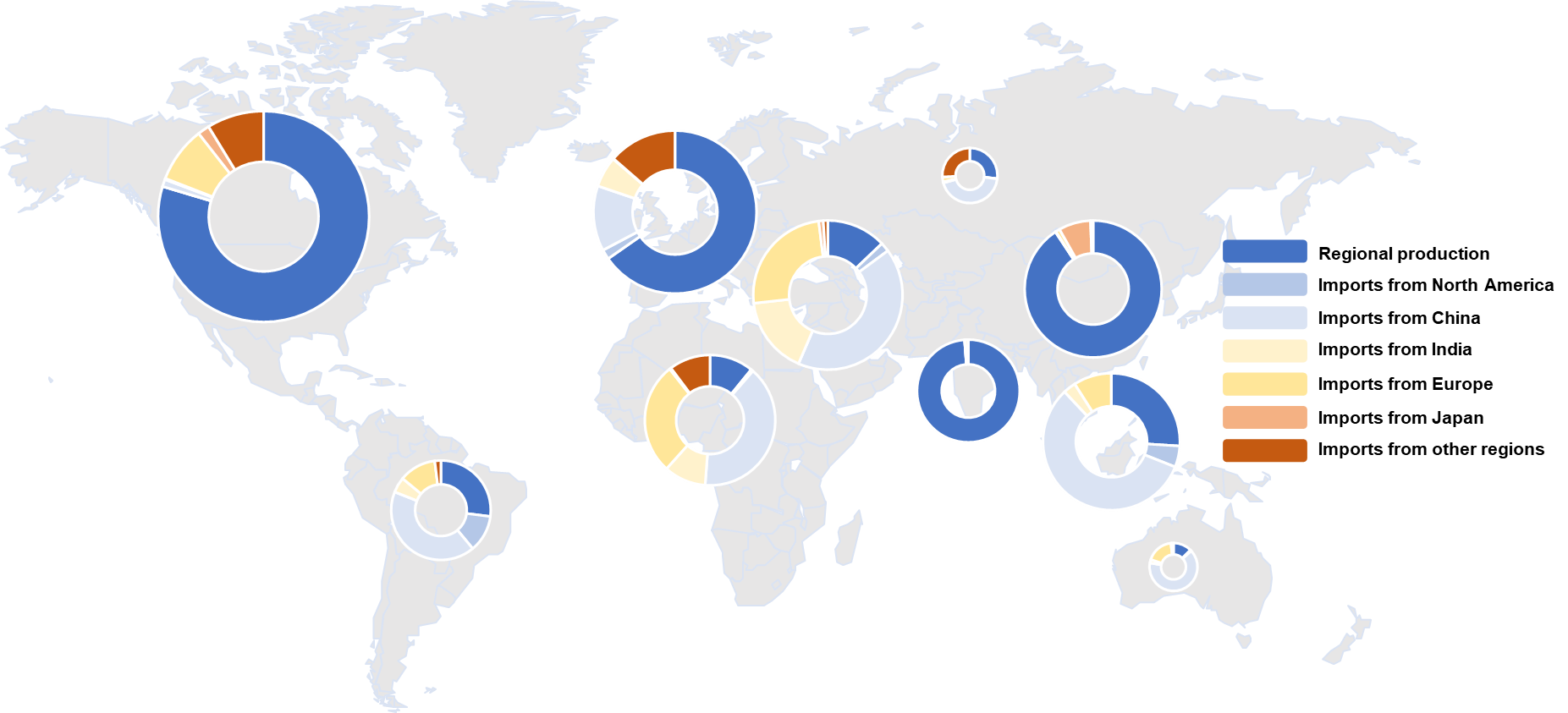

At lower kVA bands, the world's largest regional markets are dominated by local producers, most of them sourcing major components locally.

China and India, which account for around a quarter of the entire global opportunity from 7.5 - 1500 kVA, are supplied almost entirely by local production. Most of this is local OEMs, but some of it is accounted for by global OEMs producing in-country: in both China and India, around 10% of the market from 7.5 - 1500 kVA is accounted for by global OEMs.

In North America, where more than 80% of the market is served by local producers, almost all local production is by US-based OEMs.

In Europe, around 60% of the market is served by regional producers. Five years ago, this was closer to three quarters of the market and some of this change is attributable to higher imports from China. We estimate around half of Chinese imports to the region are accounted for by global OEMs producing in China and exporting to Europe, the balancing figure being Chinese OEMs often using "western" branded components sourced in China.

Over the last 10 - 15 years there's been a trend towards more regional production in Africa and Middle East. Across all power bands from 7.5 - 1500 kVA, we place this at around 10 - 15% of the market, rising to around a quarter of the market at power bands from 7.5 - 250 kVA. Many of these in-region producers are independently owned and working closely with major global engine and alternator OEMs. In both regions, imports from both China and India have been growing.

Imports from China to Africa and Middle East are attributed partly to global OEMs' producing in China. But at lower ratings, there's evidence that Chinese OEMs are growing their market position, often on the back of Chinese investment. We're also seeing growing imports from India. At ratings closer to 1,000 kVA, we believe a majority of these are attributable to global OEMs producing in India. But across the board and particularly at lower ratings, we're seeing a growing market presence from Indian OEMs.

The rest of the Asia Pacific market is dominated by imports from China with significant production still in Japan, but mainly for the domestic Japanese market.

2024 Opportunity for Diesel Generator Sets by Source, 7.5 - 250 kVA

Source: Genstat from Parkinson Associates. 2024 forecast based on Q1-Q3 data plus forecast for Q4.

Regional opportunities sized relative to each other.

2024 Opportunity for Diesel Generator Sets by Source, 251 - 1500 kVA

Source: Genstat from Parkinson Associates. 2024 forecast based on Q1-Q3 data plus forecast for Q4.

Regional opportunities sized relative to each other.

Above 1500 kVA

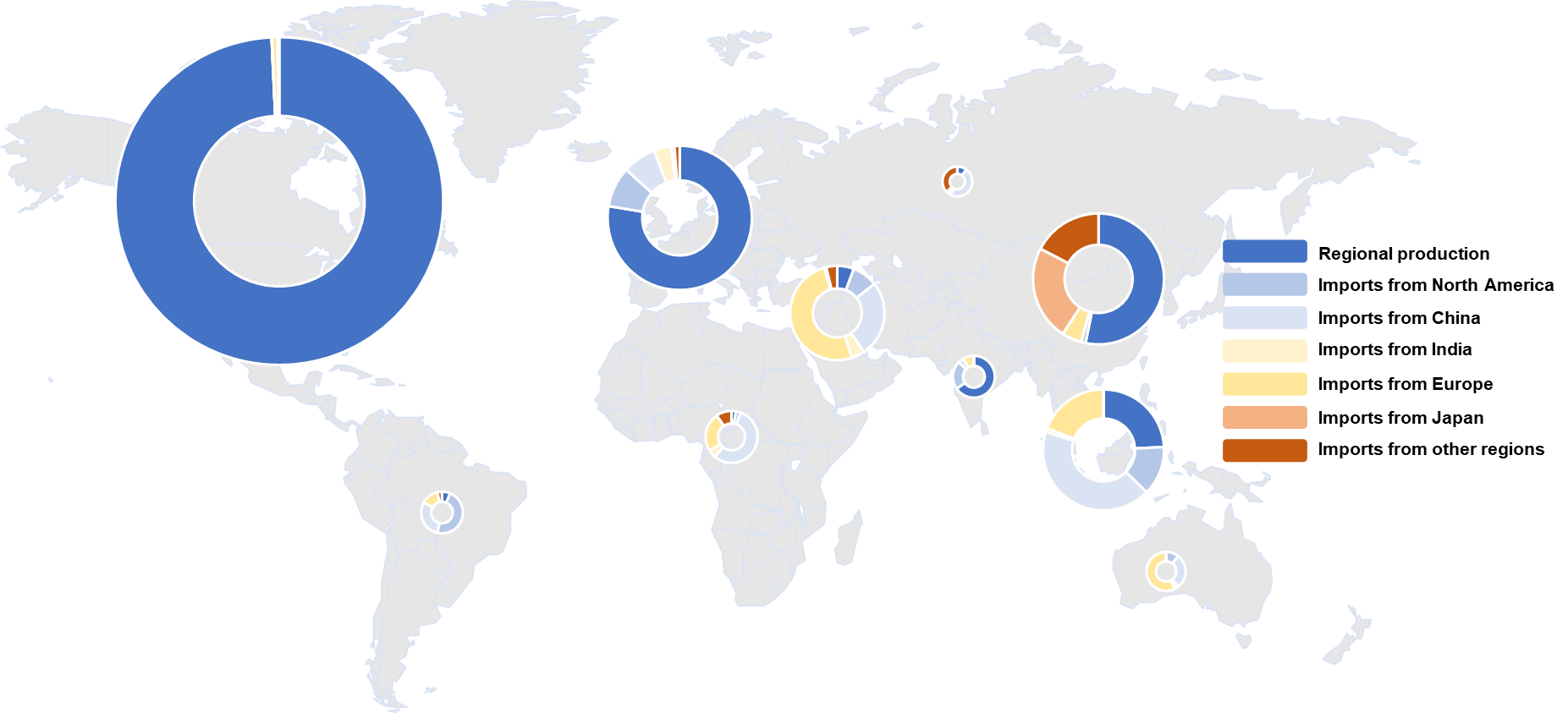

At ratings above 1500 kVA, again, the largest regional markets are dominated by local producers.

In North America, close to 100% of the market is held by in-country producers, with an almost negligible number of imports.

Around 80% of the market in Europe is held by European producers, most of them in the UK, France and Germany. These may be either independent producers or production facilities owned by major global OEMs. Imports from the US and China (most Chinese imports are by global or European OEMs) account for around 10% apiece.

In China, local production accounts for around 50% of the market and we estimate around two thirds of this is attributable to major US, European and Japanese OEMs producing in-country. These major OEMs also account for the bulk (85 - 90%) of Chinese exports to the rest of Asia at these higher power ratings.

2024 Opportunity for Diesel Generator Sets by Source, > 1500 kVA

Source: Genstat from Parkinson Associates. 2024 forecast based on Q1-Q3 data plus forecast for Q4.

Regional opportunities sized relative to each other.

India is likely to be the growing focus of attention in the next 5 - 10 years.

Looking Ahead

In today's relatively uncertain economic environment, looking ahead is fraught with potential traps.

But the market data can help point in a general direction.

What's likely to stay the same

There are some things that aren't likely to change. The markets in North America, China and India and, to a slightly lesser extent, Europe have been and will continue to be supplied primarily by local producers. China is likely to remain a major production powerhouse for the wider global market, although it's possible that it may be nearing its peak.

Equally, at higher power ratings, particularly above 2000 kVA, sourcing of diesel generator sets isn't likely to change much in the next 5 - 10 years. There are relatively few producers at these ratings, and many of them are investing heavily to grow existing capacity.

What may change

India is likely to be the growing focus of attention in the next 5 - 10 years. The country is a very sizeable market, especially at lower power ratings, and has a data center sector which is likely to see rapid growth. It's dominated by local OEMs, but increasingly, many are looking towards export markets for growth, not just in Asia Pacific but also in Africa and Middle East. Expect to see them take on a greater presence outside India in the next 5 - 10 years.

Expect more global OEMs to establish a greater manufacturing presence in India, mostly for export. The country has a growing number of global component suppliers, a strong tradition of engineering and a well established industry for diesel generator sets.

On a smaller scale, and particularly in Africa and Middle East, expect more in-region production at lower power bands, especially below 250 kVA, from locally established producers working with major component OEMs.

Insights on Opportunity for Producers of Diesel Generator Sets

To find out more about this study, contact us at at enquiries@parkinsonassociates.com

Parkinson Associates publish an opportunity database, Genstat, available quarterly and annually, for diesel generator sets, split by 12 power bands for every country. Click here to find out more.

To find out more about our research in the diesel generator set industry, click here

Download this article as a pdf