Market Drivers

in the diesel generator sets industry

in the diesel generator sets industry

July 2024

The industry for diesel generator sets doesn't have a single playbook for producers or distributors. A business model that works well in one part of the market may not work so well in another.

Here we take a high level view of the numbers and drivers and look at what sets the scene for success.

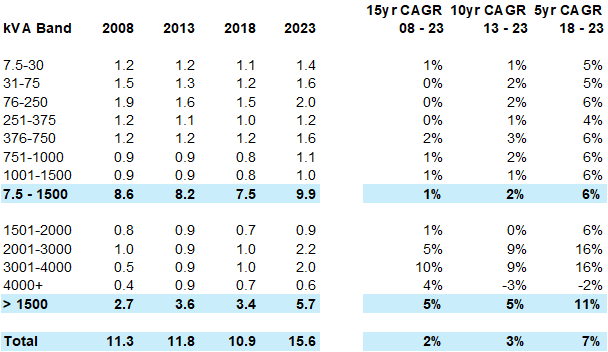

A Two-Speed Market

There has always been a dividing line in the market for diesel generator sets. A line separating the smaller, more standard, ready-to-run, off the shelf products from the more complex products which often form part of complete power systems.

Twenty or thirty years ago, that line was probably around 1,000 kVA. Now it's probably around 1,500 kVA and arguably getting closer to 2,000 kVA.

The most obvious difference between the market above and below this point is in how it's growing. In the last five years, the market above 1,500 kVA has grown at double the rate. And diesel generator sets between 2,000 and 4,000 kVA have seen five year CAGRs of 16%.

Demand for larger units has surged with growth in critical applications, especially data centers, while demand for smaller units has come from a multitude of regional events, some foreseen, others unforeseen.

There's a different playbook for success above and below this demarcation line. And the differences become much more obvious the further you move away from the demarcation.

Global Diesel Generator Sets Opportunity (US$ B)

Source: Genstat from Parkinson Associates. Values based on OEM ex-works. Includes price inflation.

Below 1,500 kVA: Efficiency, Cost and Reach

This is where the market is at its most competitive and unforgiving.

Fragmented Customers

There are a vast number of buyers and a multitude of market sectors and applications. There are a few large purchasers, for example telecoms operators or rental fleets but most customers are often small businesses and difficult to find. There is a high level of fragmentation by applications, needs and geography.

Opportunities are widely spread, difficult to identify and buyers are likely to be infrequent or reluctant purchasers. Most marketing activity is geared towards bringing customers to distributors and to access the market, manufacturers need to establish broad and active distribution coverage. This is a difficult and time-consuming exercise.

At lower power ratings, customers are highly fragmented by application and location and are often difficult to find.

High Competitive Intensity

There is a high level of competitive intensity at lower power ratings and this is where most competitors are concentrated. Premium global players jostle alongside aggressive, low cost, regional manufacturers.

Because there are only a limited number of core component suppliers, many producers of generator sets sell products with identical core components, particularly engines and alternators. And at lower power ratings, for many customers the brand of engine in a generator set is a big decider. Although there is scope to capture value on package design, for example enclosures, there's a ceiling to how much price can be captured for it. This makes product differentiation difficult and means that lower cost operators often resort to price disruption to grow business.

While global players work hard to develop and grow their own brands, often regional players sell on the strength of the engine brands inside them, particularly the engines, and rely on the aftermarket support network of the engine supplier.

Many smaller regional producers take a very flexible and reactive approach to component sourcing, shopping around for lowest cost components, quickly taking advantage of exchange rates and deals. Larger, more structured producers find this much more difficult, with more rigid processes and system / support issues to manage.

It's often difficult to be profitable from sales of generator sets alone, particularly at the lower ratings. Smaller regional players can be profitable with locally-provided added value. Larger players focus on services around generator sets.

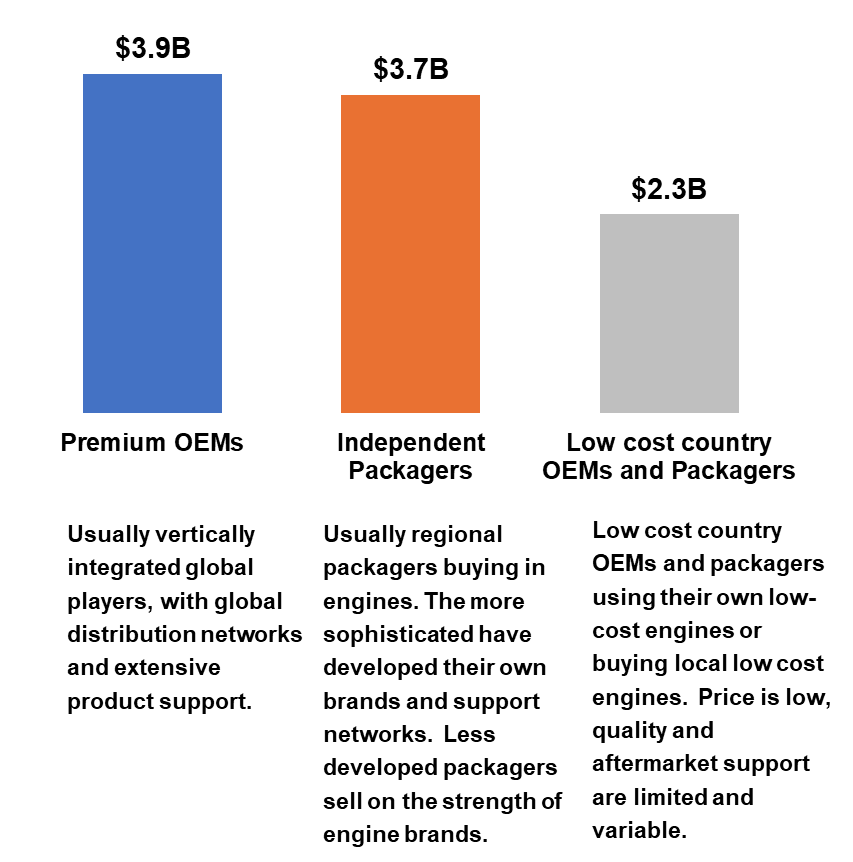

Global Opportunity by OEM Type 7.5 - 1,500 kVA (2023)

Source: Genstat+ from Parkinson Associates. Data derived from analysis of trade statistics of producing countries and production data.

New Technology

In some regions at lower power ratings, there is evidence of renewables and energy storage impacting sales of generator sets. But for now this remains a mid - long term threat or opportunity, depending how you view it.

Generator sets will continue to evolve both in terms of efficiency and usage of cleaner fuels. For the foreseeable future, it's likely that they will continue to co-exist with power generation technologies.

New Market Entrants

For many new entrants into the industry, barriers to entry may initially appear low. The market is huge and product technology is well established. But it's not that simple.

At lower power ratings, because core product margins are usually tight, it's a business where economies of scale are king. And to get to that level of scale, producers need:

Wide distribution coverage.

Products designed and priced to attract that distribution.

And the ability to offer adequate product support through distributors to maintain credibility with customers.

Competitive lead times and local inventory are key. With generator sets at lower ratings, many customers want to drive in and drive away with a product.

Putting in place a trained distribution network in place takes time, patience and investment. And this represents a significant hurdle for new entrants.

Key Success Factors < 1,500 kVA

Products priced to attract distribution partners: removing costs that don't create value.

Distribution channels that are active, efficient, cost-effective and widespread.

An efficient product support organization for customers.

Solar panels at a village in Egypt. In some regions, at the very lowest power ratings, there is evidence of renewable generation and energy storage impacting the market for generator sets. But for most larger, industrial applications, diesel generator sets are the go-to option.

Above 1,500 kVA: brands and relationships

There are fewer competitors at this level. But the competition among them is still strong. And customer expectations are very high.

Demanding Customers

At these higher power ratings, there is a relatively small number of customers. Buyers are usually corporate, risk-averse and play safe with choice of supplier. Consultants often play a key role in advising buyers on specifications.

The buying process is time-consuming, complex and involves many interactions with consultants, contractors and customers, each with their own very specific needs. What happens before the sale is decisive and relationships establishing credibility are very important. Marketing is geared towards earning trust.

Projects are often for critical power applications and core sectors are data centers, healthcare, mining, banks, major buildings / infrastructure projects. Many customers are managed as key accounts and sales won and lost are easily tracked.

Critical power segments, especially data centers, are major growth drivers for generator sets, particularly above 2,000 kVA

Competition

At these higher ratings, the market is almost entirely project-based with high engineering and financial risks. A strong track record of competence is absolutely key.

Most competitors at this level are global, vertically-integrated producers and these account for around 80% of the overall market.

But competitive intensity for every project is still very strong with suppliers bidding against other competitors.

Although there is a cost-sensitive part of the market, it's easier for suppliers to promote value and services. A strong brand is essential. Many customers are conservative, often working only with brands that they know and trust.

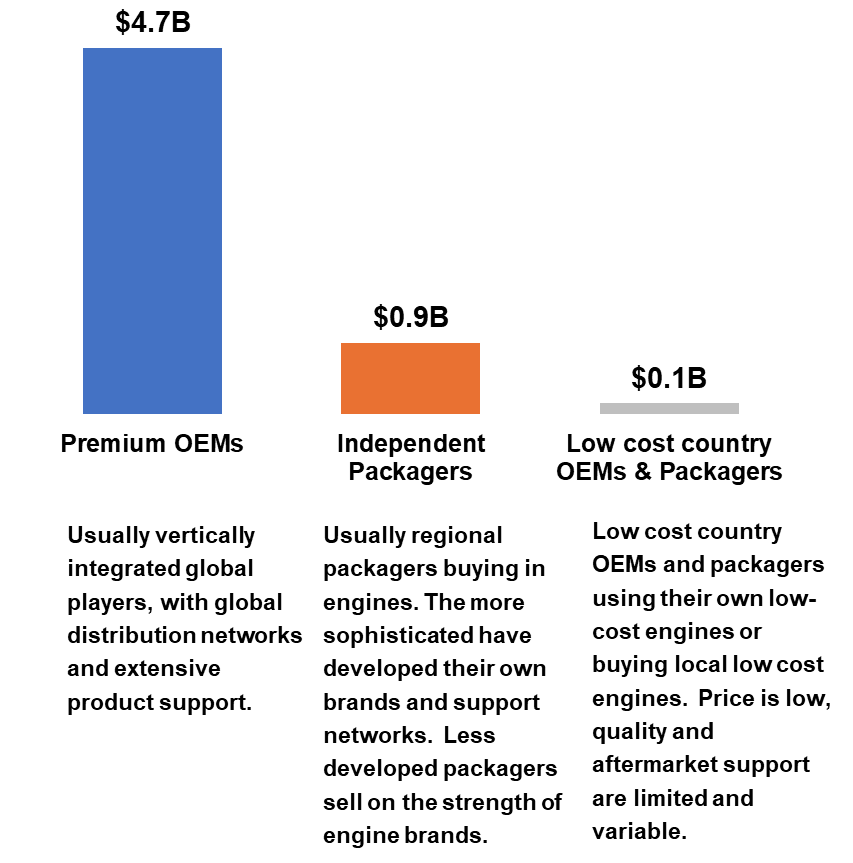

Global Opportunity by OEM Type > 1,500 kVA

Source: Genstat+ from Parkinson Associates. Data derived from analysis of trade statistics of producing countries and production data.

New Technology

Expect more sensitivity towards owning a generator set, particularly among buyer companies that represent consumer-facing brands.

But with few viable alternatives, for most larger-scale, critical power applications, a diesel generator set will continue to be seen as a necessity. Over the course of the next decade, expect to see more advances in fuel technology for generator sets, with cleaner fuel options.

At higher power ratings, diesel generator sets will also start to feature as part of wider, more balanced power systems, alongside renewable generation and energy storage.

At higher power ratings, diesel generator sets are likely to continue to co-exist with emerging power generation and energy storage technology.

New Market Entrants

At higher power ratings, especially where an application is critical, the track record of a generator set brand is very important. The quality of generator sets and performance of the supplier are critical and many customers will only consider established brands.

Customers require strong levels of brand credibility and proven competence which act as a high wall to climb for new entrants. And this means it's very difficult and time-consuming for new entrants to establish themselves.

Key Success Factors > 1,500 kVA

A well-known and established brand with a proven track record of success.

World-class levels of product engineering expertise, project management and product support.

Product information and data that are accurate, timely and of good quality.

At higher power ratings, where applications are often for critical power, many customers seek established brands with a proven track record of success and support.

Insights on Opportunity for Producers of Diesel Generator Sets

To find out more about this study, contact us at at enquiries@parkinsonassociates.com

Parkinson Associates publish an opportunity database, Genstat, available quarterly and annually, for diesel generator sets, split by 12 power bands for every country. Click here to find out more.

To find out more about our research in the diesel generator set industry, click here

Download this article as a pdf