Players in the Diesel Generator Sets Industry

February 2024

The market for diesel generator sets has a very diverse range of competitors. We've looked at how this plays out above and below 1,500 kVA. And the outcome is that these are two very different markets.

One Market, A World of Difference

At lower power ratings below 1,500 kVA, the market for diesel generator sets is a fiercely competitive playing field, getting more competitive the lower the power rating, where it's often difficult to sell differentiation and value. Below 1,500 kVA, global industry growth in 2023 will probably be a double digit % due to shipments to Ukraine, a strong North American market and some regional power crises but the long term growth trend is closer to 4 or 5%.

At higher power ratings, particularly above 2,000 kVA it's a different story. Growth in critical power applications has surged. The long term growth trend is above 10% and growth in 2023 will probably nudge 40%. Fewer competitors play at this level, customers are more cautious and risk averse and there is a clear opportunity to sell value and competence.

We've looked at how this translates in the market. For this analysis, players have been split into:

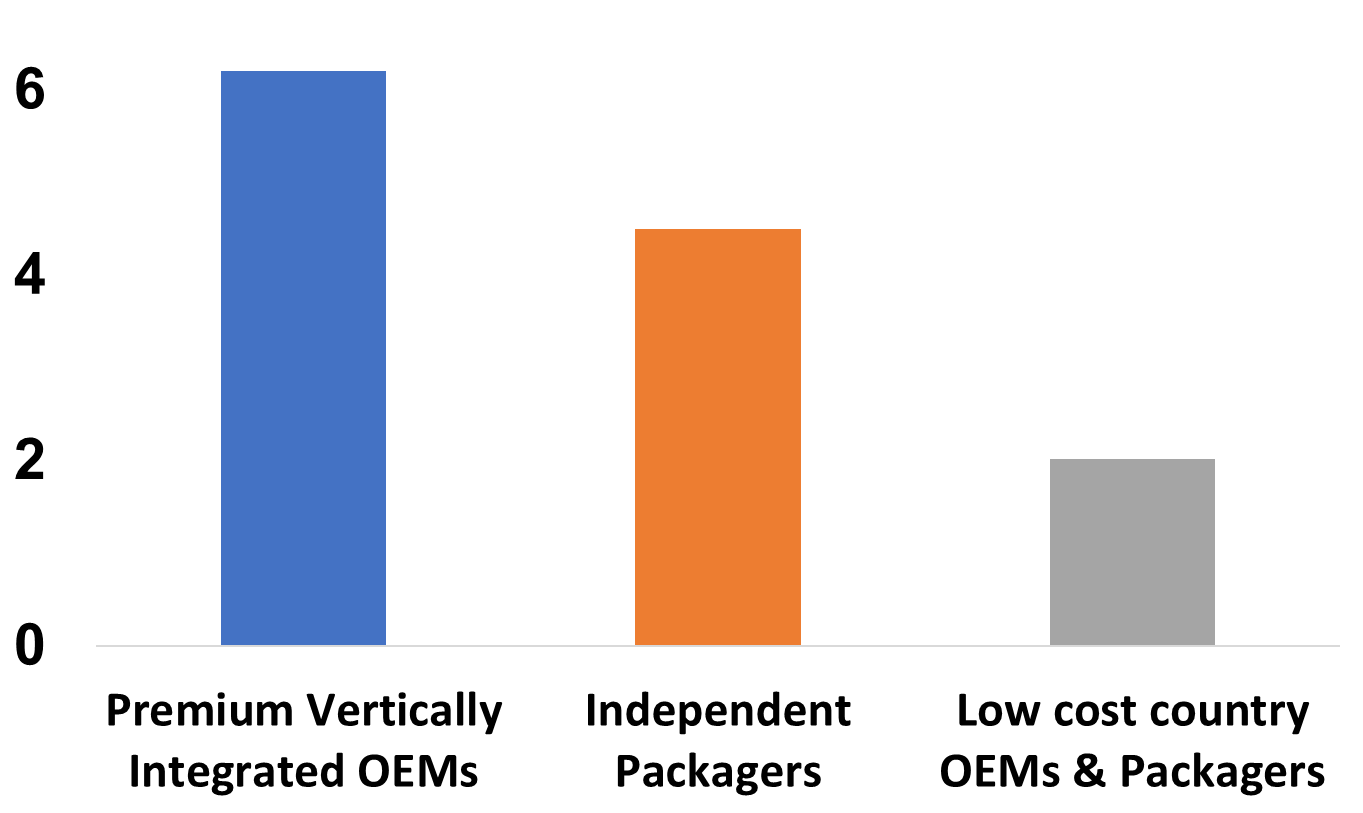

Premium vertically integrated OEMs where engines and core components usually carry the company brand.

Independent packagers, buying in engines and most other components from other OEMs.

Low cost country OEMs and packagers using their own low-cost engines or buying local low cost engines and components.

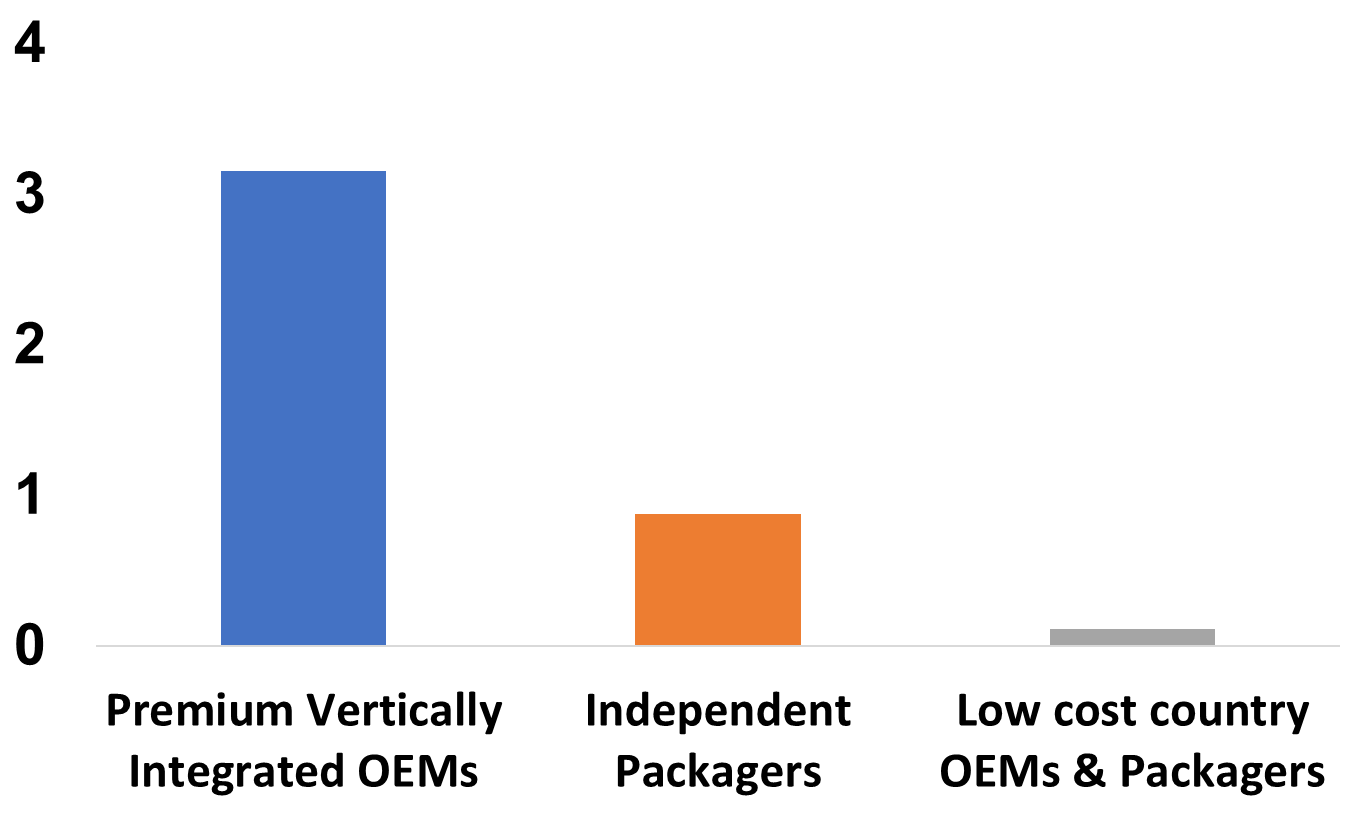

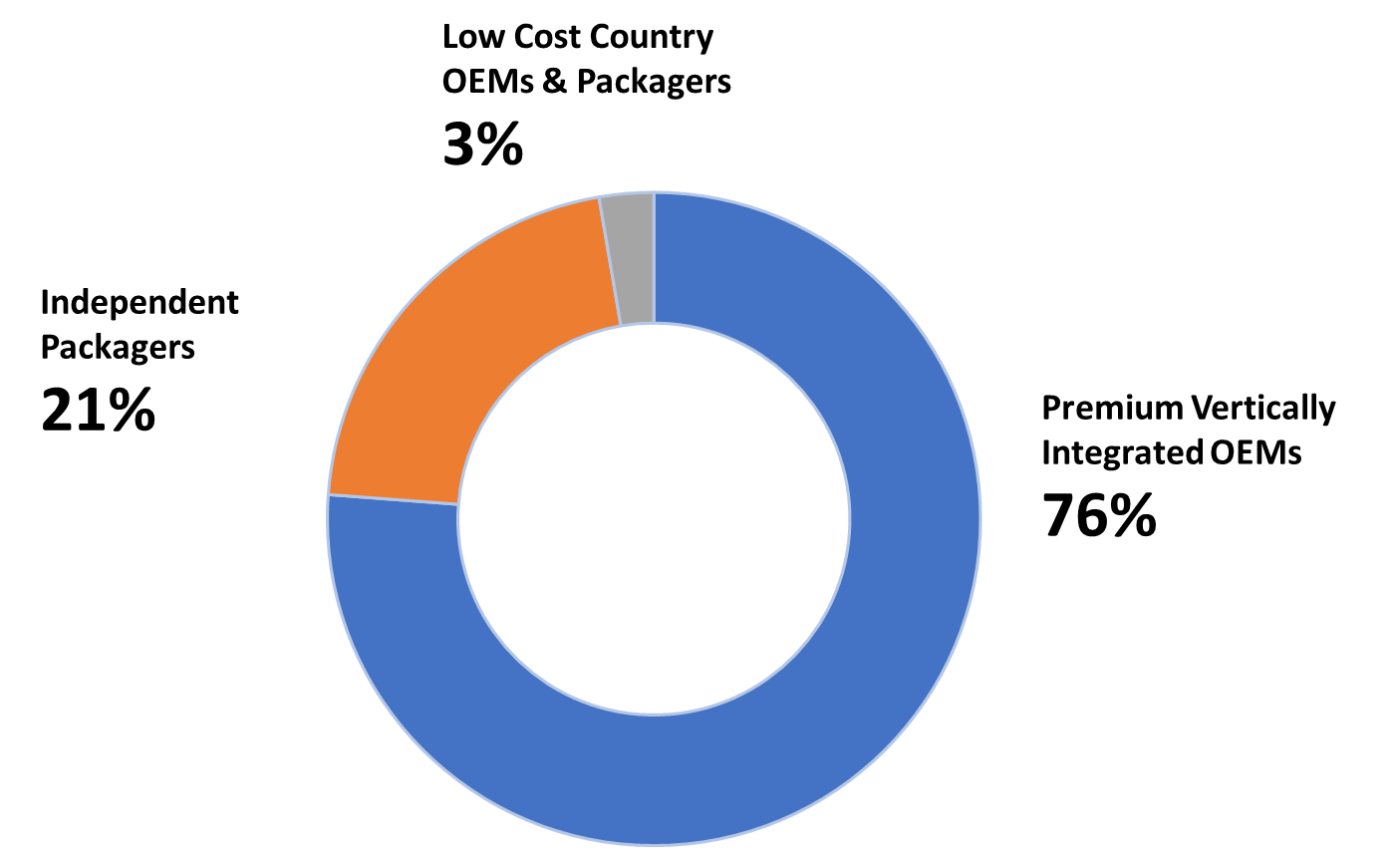

Figure 1: Global Diesel Generator Set Opportunity

by OEM Type All Power Bands (US$ Billions)

Source: Genstat+ from Parkinson Associates. Values based on OEM ex-works. Data derived from trade statistics of and analysis of production data from 2022.

From 7.5 - 1,500 kVA

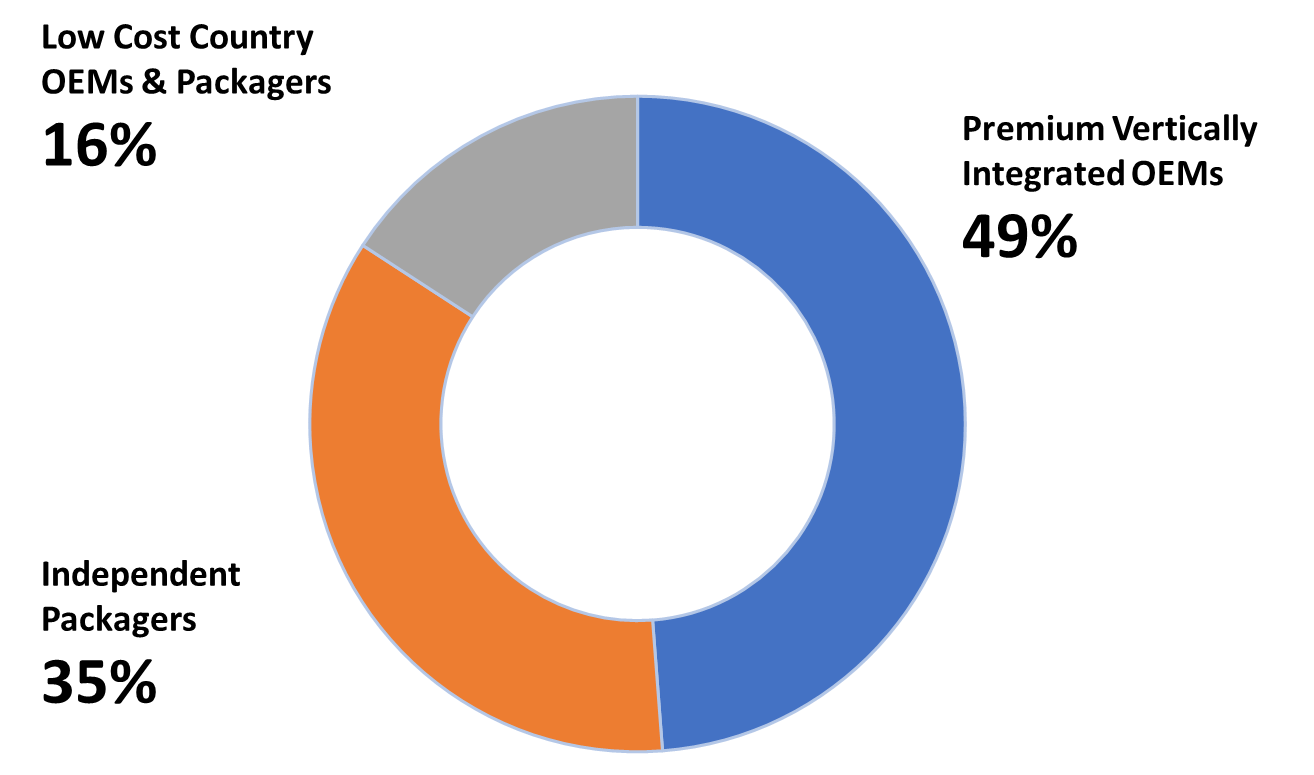

Below 1,500 kVA and particularly at lower ratings, there is less scope for brands to differentiate generator sets. Competing players offer products with very similar core components, similar capabilities and the market is price sensitive. At these power ratings, especially below 250 kVA, there's evidence that the premium vertically integrated OEMs have lost some ground to independent packagers, particularly in Africa and Middle East.

Below 1,500 kVA, independent packagers account for the largest global share of the global market. With strong control of costs and often operating on tight margins, these players are horizontally-integrated and shop around for lowest cost components, taking advantage of deals and favorable exchange rates.

Below 1,500 kVA, independent packagers dominate the European market and account for well over half of the African, Middle East, South East Asia and Latin America markets. Most of these are now local in-region packagers.

North America below 1,500 kVA is dominated by premium vertically integrated players, all assembling in-region. There are also a number of smaller independent generator set packagers with a strong localized presence.

Low cost country OEMs and packagers dominate the China and India markets and account for around a quarter of South East Asia but have negligible presence in North America and a low single digit % share in Europe, Africa, Middle East and Latin America.

Figure 2: Global Diesel Generator Set Opportunity

by OEM Type 7.5 - 1,500 kVA (US$ Billions)

Source: Genstat+ from Parkinson Associates. Values based on OEM ex-works. Data derived from trade statistics of and analysis of production data from 2022.

Above 1,500 kVA

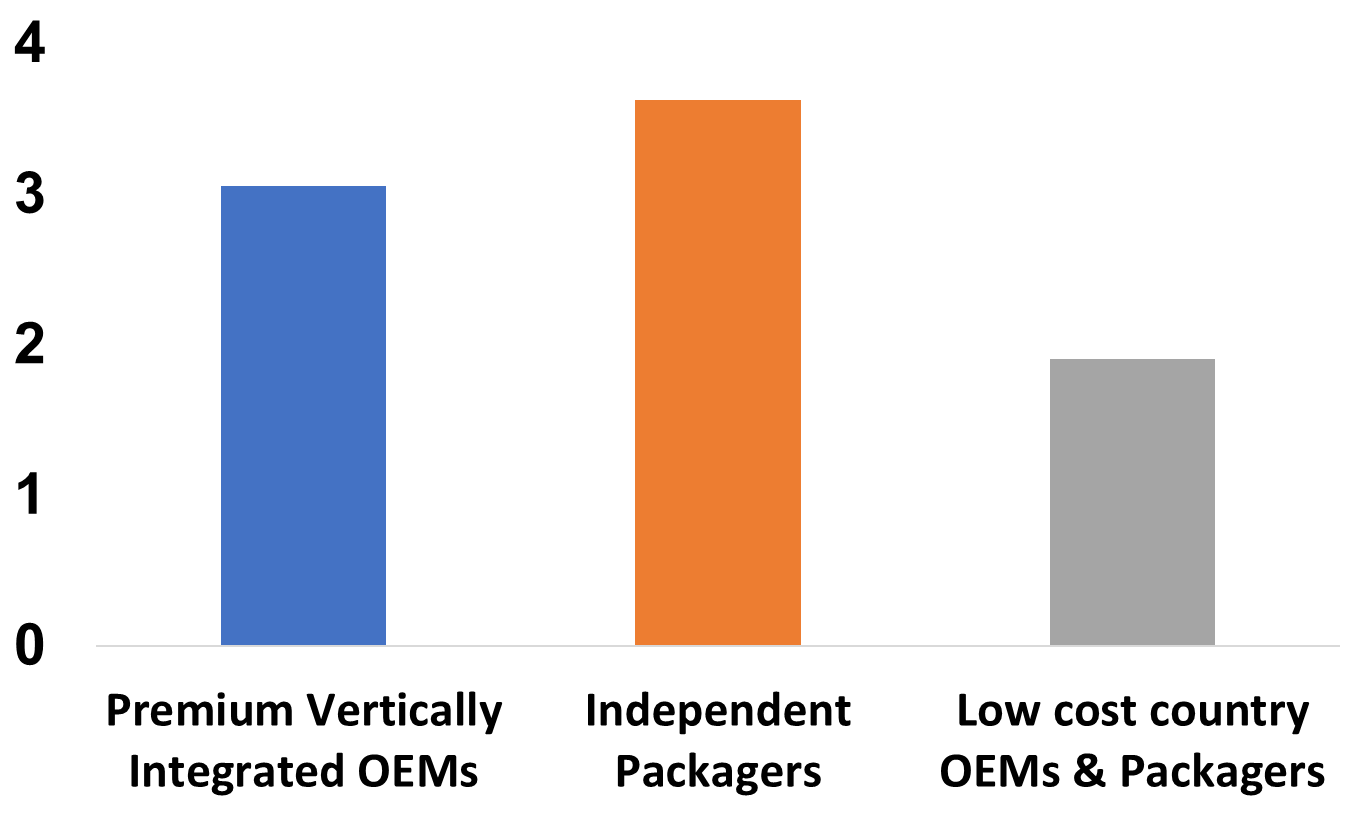

Above 1,500 kVA, the competitive landscape is very different.

Projects are more complex with a significant degree of risk, both engineering and financial, which raise the high barrier to market entry. The market is dominated by a handful of large, well established global premium players offering high levels of engineering expertise and support.

Critical power applications, particularly data centers, account for a significant proportion of the market at these ratings and customers are often very risk-averse and play safe with their choice of supplier.

Most buyers are purchasing for their business or for their employer’s business and require strong evidence of supplier credibility and proven competence. Relationships are important.

Although there are fewer players at these higher ratings, competition among them remains strong. And the recent boom in the data center sector has created some industry capacity issues which have allowed some independent packagers to grow market share.

Figure 3: Global Diesel Generator Set Opportunity

by OEM Type > 1,500 kVA (US$ Billions)

Source: Genstat+ from Parkinson Associates. Values based on OEM ex-works. Data derived from trade statistics of and analysis of production data from 2022.

Insights on Opportunity for Producers of Diesel Generator Sets

To find out more about this study, contact us at at enquiries@parkinsonassociates.com

Parkinson Associates publish an opportunity database, Genstat, available quarterly and annually, for diesel generator sets, split by 12 power bands for every country. Click here to find out more.

To find out more about our research in the diesel generator set industry, click here

Download this article as a pdf